Volume 6: Health Insurance, Part III

- Jan 31, 2017

- 9 min read

Obamacare: The Long War

“I’m not on Obamacare. My health insurance is through the ACA.” – Twitter, various

Almost seven years after its passage, the Affordable Care Act hasn’t become any less controversial. Historically, after they are passed, most pieces of legislation “settle down” into implementation mode as even opponents try to make the law work as well as possible. Not so here – from the day of its passage, its opponents have tried to dismantle the so-called “disaster”, while its proponents have refused to consider going back.

How do we best consider the effects of this complex law? Rather than making value judgments about how our health insurance system should work, let’s judge the ACA by the terms of its debate. What did its supporters predict? What did its opponents predict? Who was right? The debate over what features are present in a strong health insurance system is unlikely to end soon. But this framework should give a more neutral point of view to explain what the ACA’s effects have been.

What did the proponents of the ACA predict?

What did the opponents predict?

How is each side describing the current state of the health insurance system?

What did the proponents of the ACA predict?

Before we dive in, let’s set some ground rules. Most importantly, it would be easy to cherry-pick people on either side making crazy predictions and then shoot them down. Everything here is intended to be representative of the larger debate. For some predictions I’ll use a quote, while others have general statements.

Like my fact-checking compatriots, we’ll also need a consistent set of rulings to “rate” how everybody did. Politifact’s system seems to cover most bases. One clarification – I’ll use “Pants on Fire” only for a deliberate fabrication; an honestly made prediction that didn’t bear out is just “False”. Let’s dive in…

“If you like your plan, you can keep it." - Barack Obama

Might as well get our hands dirty right away. The President should not have made this statement – it was a promise that he had no way to keep. One of the reasons why the ACA was created was that many people with insurance were not really covered. As an extreme case, “mini-meds” were very inexpensive but had annual benefit caps as low as $2,500. Of course, some people “liked” these plans, and they were going to go away.

As discussed in previous Volumes, the ACA created various criteria, without which an insurance plan would be “non-compliant.” A significant percentage of plans on the individual marketplace lacked these conditions, and their policyholders received notification that their plan would be cancelled. While the exact number of people affected isn’t known, a good guess is that 2.5-3 million people received cancellation letters.

The White House seemed genuinely surprised by how many were affected and took action. Existing plans were grandfathered through 2017, although some providers unilaterally canceled their plans sooner (individual market plans were frequently cancelled in the pre-ACA world).

Rating: FALSE. I disagree with Politifact’s “Pants on Fire” because I think the statement was made in good faith.

Approximately 26 million people will gain coverage by 2016. - CBO

In 2012 (following the Supreme Court decision in NFIB v. Sebelius), the CBO predicted that 26 million additional net persons would be covered due to the ACA. This included:

10 million additional due to Medicaid/CHIP expansion

23 million additional on exchanges

5 million fewer by employers

2 million fewer in nongroup (i.e. individual) market

This would leave an uninsured non-elderly population of 30 million.

To see how this compares with the results, we can refer to the ACA Signups Healthcare Coverage Breakout. The categories don’t agree exactly with the CBO, but to get an idea:

Medicaid/CHIP expansion has added 14 million beneficiaries

Exchanges have added 11 million, but there are also 7 million off-exchange policies

I’m not able to make a good comparison on the nongroup or employer section with the data I have. However, with total uninsured at 29 million, the total change is in line with the CBO prediction.

Rating: TRUE. The mixture is off, but the overall number is dead on. It looks like fewer people than expected left their employer sponsored plan.

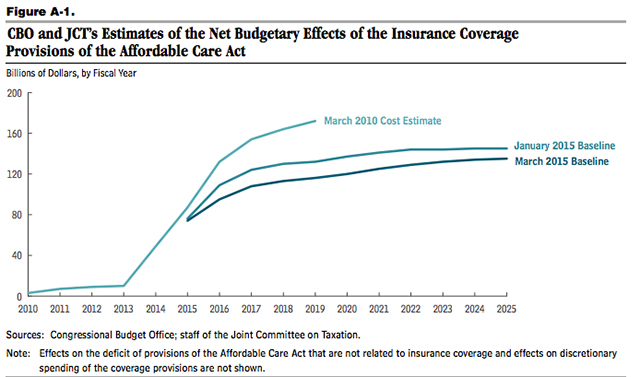

“I will not sign a plan that adds one dime to our deficits – either now or in the future.” - Barack Obama

With the caveat that it is difficult to know what would have happened without the ACA, and we don’t know what will happen in the future, the evidence is strong that the national debt is and will be smaller because of the ACA.

First, we can look at the CBO’s projection for the law; it showed a significant benefit from the ACA:

Then we can see that future CBO revisions have shown consistent reductions in the cost of the ACA:

Why have ACA costs come in lower than expected? Mostly because the costs of premiums on the exchanges are lower than expected (more on this to follow).

Rating: MOSTLY TRUE. It looks good so far, but the full law has been in effect only 3 years. The prediction stated “in the future”, so let’s be cautious.

What did the opponents predict?

“The bill’s tax hikes are a job killer…individual mandate is a job killer…employer mandate is a job killer.” - John Boehner

An incredibly common prediction about the ACA was that it would “kill jobs”. In an assault on the English language, one of the many attempts to repeal the law was entitled “Repealing the Job-Killing Health Care Law Act.” There were some reasons to think the ACA would hurt employment. First, some people who had previously been working primarily to obtain health insurance would willingly drop out of the market now that it became available elsewhere. Second, to avoid the mandate to provide insurance to full-time workers, some companies might reduce employment or move full-time employees to part-time status.

Since the passage of the ACA, there has been job growth every single month; this is a record, 70+ months and growing. In addition, there is no evidence of significant movement of full-time employees to part-time status. This isn’t to claim that the historically strong job growth over the past seven years is because of the ACA. However, Speaker Boehner said that the ACA would “kill jobs” and it hasn’t done so.

Rating: FALSE. There is no way to conclusively prove the ACA’s effect on employment. But you’d think something would have shown up by now if it was a “job killer”.

“The America I know and love is not one in which my parents or my baby with Down Syndrome will have to stand in front of Obama's 'death panel'” - Sarah Palin

I know I promised not to cherry-pick, but the idea that the ACA would lead to the government involvement in individual health care decisions was common among its opponents – this is just the most quotable.

We can dispense with it quickly. This could have been referring to the Independent Payment Advisory Board, one of the cost control mechanisms in the ACA. It was created to consider what types of treatments were effective and which were simply expensive. Or it could have been about the end-of-life counseling, which insurance companies were now required to provide (although its use is voluntary). Either way, you don’t need to worry, because as you may have noticed, no bureaucrats are making life or death decisions about your family members.

Rating: PANTS ON FIRE. Opponents were telling people that the ACA was going to kill their babies and grandmothers.

“The whole scheme is enlisting young adults to overpay, so other people can have subsidies.” - FreedomWorks

Before the ACA, a lot of healthy, young people had insurance and paid less than what they pay today. Some of this is inevitable: if we want to cover non-wealthy sick people, either wealthy people or healthy people will have to pay more (in the ACA, they both pay a bit more).

I can qualify this and claim that even the “Young Invincible” are better off. The more-expensive insurance they have today generally provides more coverage. It guarantees the essential health benefits, has no lifetime caps, can’t deny coverage due to rescission and so on. Also, the person in question might one day become old or sick; the ACA ensured that you can always get insurance.

Rating: HALF TRUE. Without context, it is misleading. But it is true that benefits to the young and healthy are long-term, while the costs are today.

How is each side describing the current state of the health insurance system?

“You have to remember this law is getting much worse. It is what actuaries say, 'Entering a death spiral.' " - Paul Ryan

The cost of premiums on the exchanges have been a major point of debate. However, the headline prices of policies, reported breathlessly in the press, affect only a small portion of the market – the less than 1% of the population who get coverage unsubsidized through the exchanges. Otherwise, the extra cost is paid by the government via exchange subsidies. So, when you see premium increases quoted in the press, remember that it is mostly affecting the amount spent by the government. So the real question is: has the government’s subsidy cost per enrollee been / will it be higher than expected? This is easy to check – we have the CBO reports.

Whoa – this is costing a lot less than we thought it would! But haven’t I read in the papers that the premiums are skyrocketing?

Well, like most things in health insurance the story is more complex. To summarize – at first the exchange premiums came in a lot lower than expected, probably because insurers were trying to buy market share. Now that the exchanges are established, insurers are using some pricing power to increase premiums – this is the normal operation of a functioning free market. But there is no sign that it is getting out of control.

But Mr. Ryan didn’t just say price increases – he said it was in a death spiral. We’ve talked about death spirals before – they have two features. Not only do premiums increase, but people start exiting the market, going without health insurance. We can take a quick trip over to ACASignups and see that 2017 enrollment will be higher than 2016.

Maybe Ryan wasn’t talking about the exchanges specifically – you could interpret his claim to be that the ACA was driving up premiums across the entire insurance market. But then he is even more wrong: how could exchange premiums be driving up prices if these plans are significantly less expensive than in the employer (group) market!

Rating: FALSE. It isn’t in a death spiral, rates are still significantly lower than originally projected, and enrollment is still increasing.

“The one unifying principle in the Republican Party at the moment is making sure that 30 million people don’t have health care” - Barack Obama

Repealing the Affordable Care Act is an official position of the Republican Party; it is also the position of the new President. I am not aware of any major Republican figure who is against repeal – so we can say they are unified around this. Are they unified around anything else?

Easy – there is no “unifying” Republican healthcare plan in existence today. There are a bunch of things out there – but no agreement on the “replace” portion of the slogan. Of the proposals, most are just a statement of goals or concepts without details. Leaving aside that the details are quite important, the goals and concepts conflict between these plans. There is no unity.

So the Republican Party is unified around repeal and not unified about anything else. But to rate the President’s statement we need to answer a question: would repealing the Affordable Care Act reduce the insured population by 30 million?

Rating: TO BE CONTINUED…

Sorry if you thought we might be done with health insurance reform, you are out of luck. We’ll need a whole new volume to look into the future – at changes which might happen and try to predict their results.

One claim about the ACA that we did not consider was its effect on overall health spending. I avoided this specifically because: I don’t know the answer. There is evidence both ways and we don’t know the counter-factual of what would have happened without the ACA.

But even if it has failed to “bend the cost curve”, I think that we can say that the ACA’s proponents have done a far better job of predicting what it would do. We can debate whether providing more and better insurance via federal government regulations and mandates is a good thing. But the Act has basically done what it was supposed to do, and not done what its opponents claimed it would.

As you could guess, I’ve read a lot of personal stories about their experience with the ACA. Based on these, I have little doubt that it has helped far more people than it has harmed. Its effect is to cost everybody a small amount while spreading out the catastrophic risks. That’s what insurance – of any type – is supposed to do. But, there are still people who are struggling to get care and struggling to cover its costs. The job isn’t done. One of the stories that gives me the most trouble is a Twitter conversation I came across. I encourage you to read it, it did more to concern me about the post-ACA insurance world than 1,000 politicians screaming into their microphones. So in Part IV, I’ll also give my thoughts about how to help people who are still falling through the cracks.

Comments