Volume 4: Health Insurance, Part II

- Dec 21, 2016

- 15 min read

What is Obamacare: How many legs does a good stool need?

“Obamacare is really I think the worst thing that has happened in this nation since slavery.” – Ben Carson

“Five days from now…millions of Americans who don’t have health insurance because they’ve been priced out of the market or been denied because of a pre-existing condition, they will finally be able to buy quality, affordable health insurance.” – Barack Obama

It is impossible to write about the Patient Protection and Affordable Care Act (“ACA” for short) without touching politics. Democrats have favored governmental enforcement of a right to health care for at least fifty years. Republicans have opposed governmental action at the federal level, believing the solution is best found by the market. Health insurance reform, almost by definition, will have winners and losers. Any discussion of the federal government actively increasing access to care will be a political issue.

To avoid the politics as much as possible, we will rely on our usual methodology. Look at the data, use it to build a theory, test the theory. My view is that, given a basic set of goals, any working health insurance system must have certain specific features. I think I’ll be able to demonstrate this. We’ll then look at the details of how the ACA implements this system, as well as its other features.

What is the 3-legged stool of a stable health insurance market?

How does the Affordable Care Act create the stool?

What else is in the Affordable Care Act?

What is the 3-legged stool of health insurance?

It is my opinion that, in the United States, in 2016, all people in this country should have a right to some level of health care(1). I can make an economic argument for this: better health care leads to a healthier work force, which leads to economic growth. I can make a selfish argument: if people aren’t able to get this care, communicable diseases would spread, and that is bad for me(2). I can make a moral/practical argument: we have the resources to provide this care and therefore we can and should provide it(3). The 1986 Emergency Medical Treatment & Labor Act(4) codified the principle by requiring hospitals provide “stabilizing care” regardless of ability to pay. We can debate endlessly what should constitute “some level of healthcare.” But if you disagree with me on the basic principle, then your position is that poor people with treatable conditions should literally die on the streets. Otherwise, your concern should be about how to provide this care and how to pay for it, fairly and efficiently.

The easiest way to do so is to have the government handle the bulk of the problem. There are two basic ways a government-based health insurance system can work. In a Single Payer system, the government provides health insurance to its citizens, but care is provided by private entities (doctors, hospitals, etc). This is basically how Medicare works, as well as Canada’s system(5). In a Single Provider system, most providers work for a governmental organization. This is what the UK’s National Health Service (“NHS”) is. We’ll discuss how the US could or should move to a Single Payer/Provider in a later volume, but it would be very difficult and disruptive. So we’ll start with how to have a successful hybrid public-private system such as exists here today.

In Volume 2, we saw how an unregulated (or poorly regulated) private health insurance system will devolve into a death spiral. But there are some countries (Germany and Switzerland) that have had success by properly regulating their private insurance markets, so we know it’s possible. There are three basic provisions that are required to have a stable system. Just like any other stool, without these three legs your system will collapse(6).

The basic problem is what to do with people who are currently ill or have serious, ongoing conditions. Let’s say this group of people has “pre-existing conditions”. According to the Kaiser Family Foundation, almost half of all US healthcare spending is spent on the top 5% of users(7). Insuring this group costs 10x as much as the average population, which makes it unprofitable for insurers. If they have a choice, no insurance company would be willing to insure people with pre-existing conditions at any reasonable price. So, for-profit insurance companies create a strong screening process, denying coverage to those most likely to get sick. But what happens to the people who are denied coverage(8)? The answer is, generally, a two-step process.

First, because they can’t afford it, they do not get care, for both their pre-existing condition and new medical issues. Generally, treating health problems earlier results in both better outcomes and lower costs. When people don’t use preventative care, the system has higher costs for worse outcomes.

Then, when the issue becomes urgent, they seek emergency care. If you have ever looked at a doctor’s bill, at the top is usually an exorbitantly high price for your service. Lower, there will be the discount that the insurance company negotiated with the provider, and the net price is fairly reasonable. But the uninsured do not get access to this discount, and because these people aren’t in jobs with health benefits, most are especially unable to afford the initial, exorbitant price. So, when faced with major medical bills, they tend to declare bankruptcy. The hospital gets pennies on the dollar, but they have already experienced their own costs for the care given(9). To make this up, they raise the prices for everybody else. Bringing the uninsured “in the system” would save us all money.

This brings us to the first leg of the stool: Guaranteed Issue and Community Rating. Guaranteed Issue says that applicants can not be denied health insurance based on their health condition(10). Community Rating means premium rates depend on the population, not individual health conditions. When a policy maker says they want to keep prohibitions against pre-existing conditions, these rules are what they mean. But even with these rules, the system will still move to a death spiral. Healthy people will wait until they are sick to buy insurance, since it can no longer be denied to them. The average person with health insurance becomes more expensive to insure and premiums will increase. As premiums move higher for everybody, more healthy people will go without insurance, and the cycle repeats. We clearly need a way to keep the healthy people in the system.

This is the Individual Mandate, the second leg of the stool. An Individual Mandate, generally, requires people to carry health insurance(11). Out of all the provisions of a successful public-private health insurance system, the Individual Mandate is the most controversial and unpopular. Why should you have to buy health insurance if you don’t want it?

But an insurance mandate shouldn’t be a new concept to you. If you own a car, you are required to carry car insurance(12). The idea is simple. Anybody can get into an accident, even the best drivers. Accidents cause damage to cars, people and property. Damage costs money to repair. Drivers of cars in accidents are liable for the cost of repairing this damage. Some accidents cause damage with catastrophic repair cost; most people can’t afford these costs and would go bankrupt if forced to pay them. So drivers are required to carry car insurance, which solves this problem. In case I’m not being pedantic enough:

Anybody can get sick, even the healthiest people. Sickness causes damage to your body. The damage costs money to repair. People are liable for the cost of repairing this damage. Some sicknesses cause damage with catastrophic repair cost; most people can’t afford these costs and would go bankrupt if forced to pay them. So people must carry health insurance, solving this problem, which otherwise hurts society as a whole(13).

This brings us to our third leg. We have required insurance companies to take all comers, and required all people to carry insurance. But, we have done nothing to ensure that this insurance is affordable. Given that the people who don’t currently health insurance tend to be of below average income, this is a real problem. The solution is Subsidies; the government pays money towards the purchase of health insurance. These Subsidies are usually progressive based on income, but you can envision systems where they are the same for everybody.

This is the 3-legged stool of a stable public-private health insurance system: Guaranteed Issue + Community Rating, Individual Mandate, Subsidies. The system will not work if any of the legs are removed:

A system with Community Rating but no Mandate will death spiral as people wait to buy insurance. Subsidies would slow down the spiral, but not prevent it.

Community Rating and Mandate without Subsidy will require people who legitimately can’t afford insurance to buy it. The math doesn’t work.

Mandate and Subsidy without Guaranteed Issue means that you are requiring people with pre-existing conditions to buy health insurance and even helping them to pay, but nobody will sell to them. This is nonsense (even if it is subsidized).

How does the Affordable Care Act create a stool?

At its core, the ACA is a straightforward implementation of our stool. But, because the goal was to affect the existing system as little as possible, the actual manner in which it builds the stool has a few complexities.

Guaranteed Issue + Community Rating:

Guaranteed Issue is created in a straightforward manner in the individual market. Insurance companies are required to both 1) accept for coverage any individual who applies and 2) accept renewals for any current policyholder, with limited exceptions(14). Community Rating creates specific factors that may be considered in determining premiums, and creates maximum premium “bands” for these factors(15). So far, so good.

Individual Mandate:

The Individual Mandate is not as simple. Rather than a requirement to hold insurance, the ACA’s Individual Mandate is a tax, collected by the IRS(16), against those who do not hold coverage(17). However, given that the penalty ($695, with adjustments for inflation) is less than the cost of buying insurance, some healthy people will voluntarily remain uninsured and pay the penalty. This is a problem – it worsens the insured pool(18).

Subsidies:

The Subsidies in the ACA scale progressively, based on household income and size, residency and cost of plans. Generally, subsidies are available for families earning up to 400% of the Federal Poverty Level (FPL). For example, a family of 4 living in Brooklyn will receive some subsidies up to approximately $97,000 in household income(19).

This is the core of the ACA. It’s not perfect– the Mandate is somewhat weak, and the subsidies are a bit low – but at first glance we appear to have created a stable 3-legged stool. It should help us to our main goal, providing access to health care for everybody, as well as a way for them to pay for it. While the government is more involved in regulation, we are still in a system based on private insurance.

What else is in the Affordable Care Act?

As you may have heard, the ACA is a long law – 1900 pages(20). Not all of this is related to the strict creation of the stool and some of it goes beyond health insurance and into health care(21).

Expansion of Medicaid

When determining the Subsidies, households that fell below a certain income threshold (138% of the FPL) were going to be subsidized for the full cost of purchasing health insurance (or nearly so). Because Medicaid provides care more efficiently than the private insurance market(22), it made sense to add these households to that existing, successful program.

Recall that Medicaid is a state-federal partnership, with the federal government paying 50-75% of the costs. The ACA said that if states increased eligibility to 138% of FPL(23), the federal government would pay for 100% of the incremental cost initially, scaling down to 90% by 2020. Astoundingly, 19 states have turned down free money from the federal government to expand Medicaid(24). Their citizens are paying increased taxes under the ACA, but not getting the benefits. I have never heard a convincing argument for a state not to accept Medicaid expansion. But hey, that’s their right(25).

Tax Increases

Between the Subsidies and Medicaid expansion, the Federal government is going to have to come up with some revenue. When designing the ACA, President Obama and congressional leaders wanted the law to be deficit neutral. Being Democrats, 21 new taxes was the bare minimum. The only one that is likely to affect you directly is a surtax of 0.9% of earned income and 3.8% of investment income on earnings above $200,000 (individuals) or $250,000 (families)(26). Netting costs and new revenues, the CBO predicted in 2010 that the ACA would reduce federal budget deficits by $124 billion over the period 2010-2019; today, they project that the ACA will reduce budget deficits by $353 billion from 2016-2025(27).

Creation of Exchanges

In order to facilitate the purchasing of health insurance, the ACA creates exchanges where individuals can shop for health plans. Each state has the option to create its own exchange or rely on the federal exchange. The purpose of the exchanges is to have a single location to compare available policies, see their costs and estimate subsidies. After a disastrous roll-out, the Federal Exchange is mostly operating well. Some of the state exchanges are excellent, while others are sub-par.

Employer Mandate

One concern about the ACA was that, with subsidized health insurance available on the individual market, employers would start to offer health insurance to fewer employees. This trend was occurring for many years, but the passage of the ACA could be expected to accelerate it. In order to prevent this, employers are required to pay penalties if they do not provide health care to full-time employees.

Young adults on Parents’ Insurance

In one of the law’s most popular provisions, young adults gained the right to remain on their parents plan up to age 26.

Medicare and other cost savings

In the passage of the ACA, there was a lot of talk about lowering the always-high rate of medical inflation. ACA cost control measures have an element of “see what sticks”; there are a lot of experimental programs, some of which will succeed and some won’t. But one major area of solid savings is Medicare. In exchange for a promise of more “customers” and fewer unpaid bills, Medicare was able to negotiate with providers (mostly hospitals) to achieve savings valued at $716 billion in the first decade(28). These savings will not decrease the services received by Medicare beneficiaries – it is the same level of care but at a lower cost.

Other insurance regulations

On top of the basic 3-legged stool provisions of Guaranteed Issue and Community Rating, the ACA imposes other minimum requirements on insurance policies. These include: policies must cover various types of preventative care; must limit overhead and profits to 20% of premiums; can not impose lifetime caps on benefits; can not include “rescission”, an especially nasty trick that used to be common; and must provide “ten essential health benefits.”

So that’s what is in the Affordable Care Act, probably the most controversial piece of legislation of the last 40 years. And yet, the basic structure of the ACA is a requirement of any stable health insurance system. At one point Republicans agreed with this concept; the conservative think tank Heritage Foundation was an early proponent of the individual mandate(29). In the 1990s, Republicans (including Newt Gingrich) supported a plan that was structurally similar to the ACA(30). And of course, the ACA is largely modelled on the health reform implemented in Massachusetts in 2006, signed by its Republican governor, Mitt Romney(31).

The fact that Republicans used to support ACA-style reform doesn’t prove that it is working. There will be at least two more Volumes on Health Insurance(32): one to discuss the results of the ACA against the expectations of its proponents and opponents and one to discuss current proposals to continue reforming the system. I’ll also write about what I would do, both in theory and in the current political climate.

Without getting to the details yet, let’s look at the insurance ecosystem today compared to 2010. In 2010, the uninsured rate in the United States was around 16.5% and increasing by around 0.5% per year. By 2014, when the major provisions on the ACA began to take effect, it had reached 18%(33).

By 2015, with the exchanges operating and Medicaid expanding, this had been reduced to 11.4%. According to a CDC survey, by Q4 2016 this has reached 8.6%, the lowest level ever recorded(34). So, on what I consider to be the core of the ACA, the law has been a success; many more people have basic access to care and a way to pay for it.

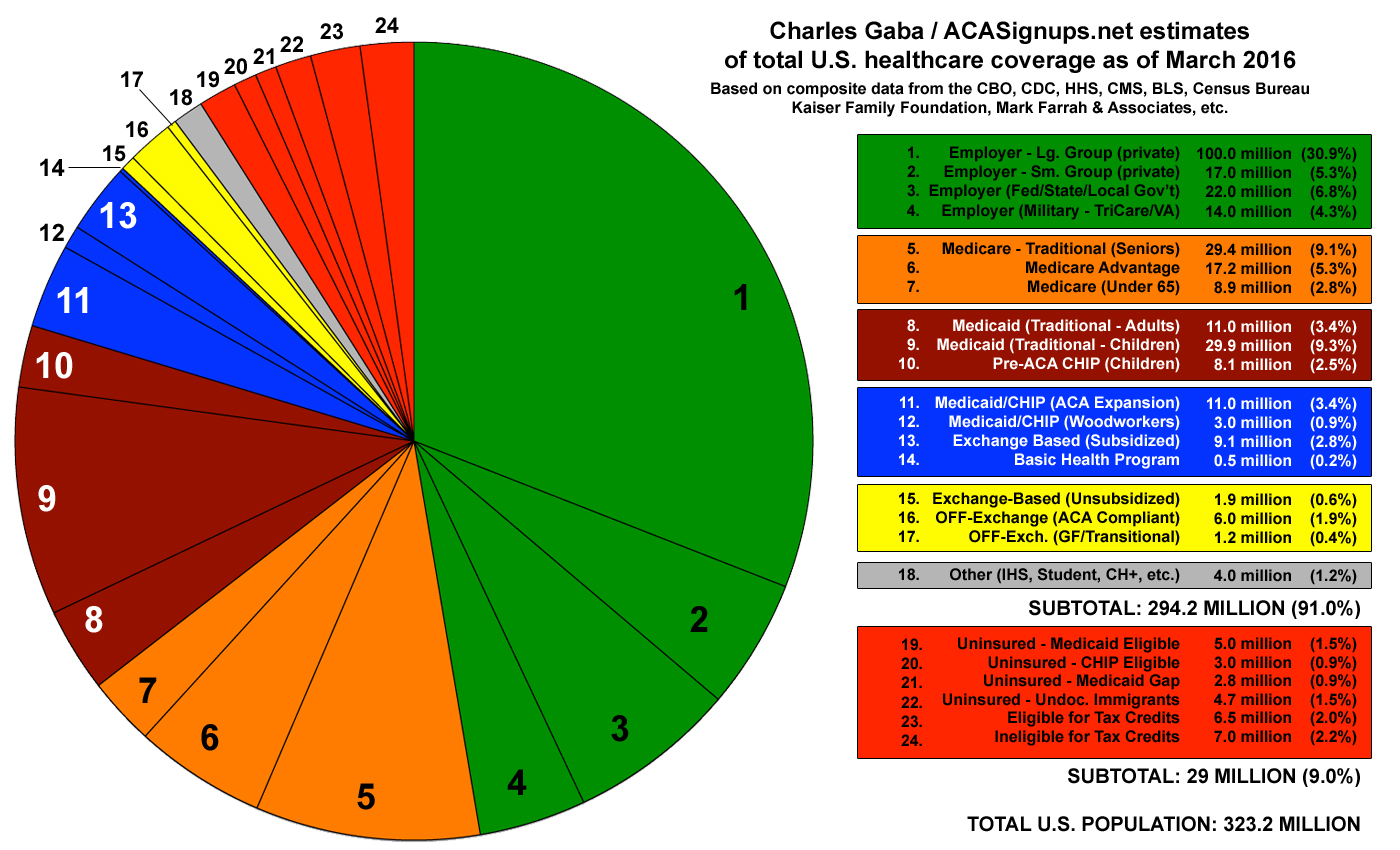

Who are the 8.6% who are still uninsured? We haven’t used ACASignups.net much yet; it is an indispensable resource and we will see it a lot more when looking at the details of what the ACA has done(35). But I’ll close this Volume with my favorite of his many great charts(36), a snapshot of the current sources of insurance in the United States. He identifies 6 main pools of uninsured:

Eligible for Medicaid, but not signed up (Medicaid still has a social stigma)

Eligible for CHIP, but not signed up

Ineligible for Medicaid due to living in a state that did not expand

Undocumented immigrants

Eligible for tax credits on the Exchange

Ineligible for tax credits on the Exchange

In later articles, we’ll look at ways to reach each of these groups.

Note the phrasing: “all people”. I’m including foreigners, undocumented immigrants and other non-permanent residents.

It’s fairly easy to list historical diseases that spread to the rich in this way: Sweating Sickness and Spanish Flu are two examples.

See Volume 2. All other advanced countries are able to provide this care guarantee while spending significantly less than we do on health care overall.

Signed by Ronald Reagan.

Whose system is also called “Medicare”. No, Canadians are not “swarming” to the US to get health care, that is a myth. Canadians face longer wait times for some procedures, especially elective ones. But they also spend about half of what we do on healthcare (OECD) – they consciously accept the tradeoff of some rationing of care for savings in the system overall.

This is my telling of the 3-legged stool, I’m not citing sources. If you care, I see 28,000 hits on Google; Krugman tells the story better than I do. This site uses a cartoon.

See here. Interestingly, this general trend is true for a lot of consumables. In drinking, the top 10% account for 50% of the total – an average of 74 drinks per week!

Or, accept, but only for care other than their pre-existing condition, e.g. an asthmatic would be covered for everything except asthma. These were called “exclusions”, and insurance companies using them doesn’t help the system.

Yes, hospitals are usually willing to negotiate their fee, but in then they are paid back only a fraction of their costs of major procedures. So we haven’t solved the problem.

According to a recent survey, 52 million adults under 65 (27%) have pre-existing conditions; this population would be uninsurable without Guaranteed Issue.

Or, similarly, to attach a large enough penalty for not carrying where it makes sense for them to carry it.

Unless you live in New Hampshire. A few other states let you post a bond or pay an uninsured motorist fee, but the concept is the same.

There are some differences between mandated auto and health insurance. First, medical problems theoretically harm only you, while a car accident damages other people’s property. But as we’ve seen, the uninsured person who suddenly decides they do want care affects all of us. Also, unlike a health insurance mandate, people do have a choice with car insurance – they could choose not to drive. So, in theory people who are opposed to insurance mandates should also be strong supporters of public transportation?

45 CFR 147.104 and 45 CFR 148.122. CFR = Code of Federal Regulation. If you really want to go down the rabbit hole, use those links to see Cornell Law’s excellent database of regulations.

One of the strangest ACA myths is that it is “run by the IRS”. This is nonsense. The Subsidies are based on income; the IRS computes Subsidy amounts based on formulas. The Individual Mandate penalty is a tax; the IRS checks to see if you owe the tax. If you don’t pay your taxes, the IRS enforces this. I am amazed I have to say this, but the IRS does not receive your personal health information (other than whether you carried insurance), and has no role in health-care decision making at any level.

The penalty is waived if a person can not afford insurance, including subsidies. This is defined as not being able to find coverage for less than 8% of household income.

26 US Code 5000A describes the Individual Mandate.

Kaiser Family has a handy site to estimate subsidies.

This is long, but our government is not efficient in terms of printing bills. I’ll use this link to the ACA text to demonstrate this – look at those margins! In word count, the ACA similar to the longer Harry Potter books. Also, bills are complex because they are usually not stand-alone laws, but rather amendments to sections of the US Code. It makes a lot of sense to have a single, consistent body of Federal Code, but it does mean that new legislation is going to be long and illegible.

There are many summaries of these provisions if you look around. Here is a short one and a long one.

I am confident to say this in this context. Again looking at Kaiser, a 1996-1999 survey showed that moving adults from Medicaid to private insurance would increase the cost by 18%; a similar 2005 survey showed a 26% increase (I’m intentionally looking pre-ACA). Here is an interesting Politifact which challenges the efficiency argument; it makes the 100% valid point that some Medicaid support is provided “for free” by the rest of the government, e.g. the IRS collects Medicaid taxes. But this is beside the point –it is less expensive for the government to provide care to an incremental person via Medicaid than by buying private insurance. If the government shares resources between departments, that’s great efficiency. And while there is mixed evidence, most surveys show that people are at least as happy with Medicaid as private insurance.

Here are charts of current Medicaid eligibility by state.

Here is more information on Medicaid expansion if you want to dive deeper.

It is literally their right, per the Supreme Court in NFIB v. Sebelius

See here. The individual mandate is another one of the 21 taxes.

Original and Current. I am taking the cost of repeal to be equal to the benefit of being in place as a good first-order approximation. I use the version without macroeconomic benefits as this the standard for CBO analysis as stated in the link. These CBO numbers are approximations, as it is impossible to know what would have happened to the country in the absence of the ACA. But as they say, there is good reason to conclude that actual benefit has been slightly better than predicted. All the evidence implies that the ACA’s effect on the overall fiscal situation is neutral to positive.

From Kaiser again. These cost savings seem to be coming in as expected, but it’s always hard to know because there is no way to run a controlled experiment.

MassHealth

An increasingly mis-named trilogy?

Per Gallup.

NHIS survey.

Randomly, I went to the same high school as Charles Gaba, who runs ACA Signups.

Original version here with methodology.

Comments